From CNBC — By Kate Dore —

Many retirees don’t think about taxes until it’s time to withdraw funds from a pretax account, which can be a costly mistake, financial experts say.

Only 3 in 10 Americans have a plan to reduce taxes on retirement savings, according to a Northwestern Mutual study from January that polled roughly 4,600 U.S. adults.

However, the “bucket strategy” is one way to minimize that burden, according to certified financial planner Sean Lovison, founder of Purpose Built Financial Services in the Philadelphia metro area.

You can reduce your lifetime tax burden by strategically receiving more income in lower-earning years to fill your “buckets” or federal tax brackets, said Lovison, who is also a certified public accountant.

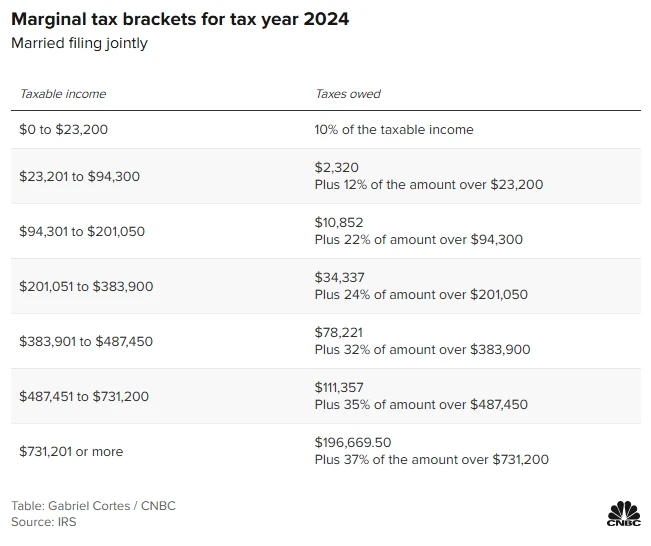

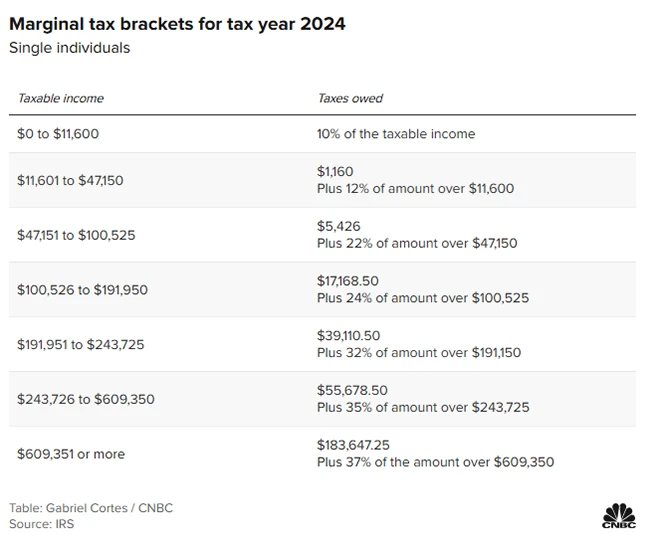

For example, if you’re in the 12% tax bracket before collecting Social Security, that could be a chance for Roth individual retirement account conversions to save on taxes later, he said.

Roth conversions transfer pretax or nondeductible IRA money to a Roth IRA, which won’t incur levies on future withdrawals. The trade-off is upfront taxes on your converted balance.

You could reduce pretax balances by converting enough to put yourself in the 22% or 24% tax bracket. Otherwise, you could be in the 32%, 35% or 37% tax bracket once Social Security and required minimum distributions, or RMDs, kick in, Lovison said.

Secure 2.0 pushed the beginning date for RMDs to age 73 starting in 2023 and that age jumps to 75 in 2033. Meanwhile, pretax 401(k) and IRA balances are growing.

“That’s a real issue right now that people don’t really think about,” Lovison said.

Focus on taxes in the ‘accumulation phase’

Often, investors don’t think about taxes until they start making withdrawals from pretax retirement accounts, said CFP Judy Brown at SC&H Group in the Washington, D.C., and Baltimore area. She is also a certified public accountant.

“They thought they had $1 million in their 401(k), but really it’s only $700,000 after taxes,” she said. “A lot of people see the value of tax planning when they get to that distribution.”

However, tax planning is key during the “accumulation phase,” as you’re growing your nest egg. Adding to pretax, Roth and brokerage accounts can provide “tax diversification,” Brown said.

Those accounts will provide “a lot of different levers to pull” to better manage your adjusted gross income in retirement, she added.

Reach us by phone at 419-756-3211, email to kmm@kmmcpas.com, or by filling out the contact form on this website here.